Industry research

Scope

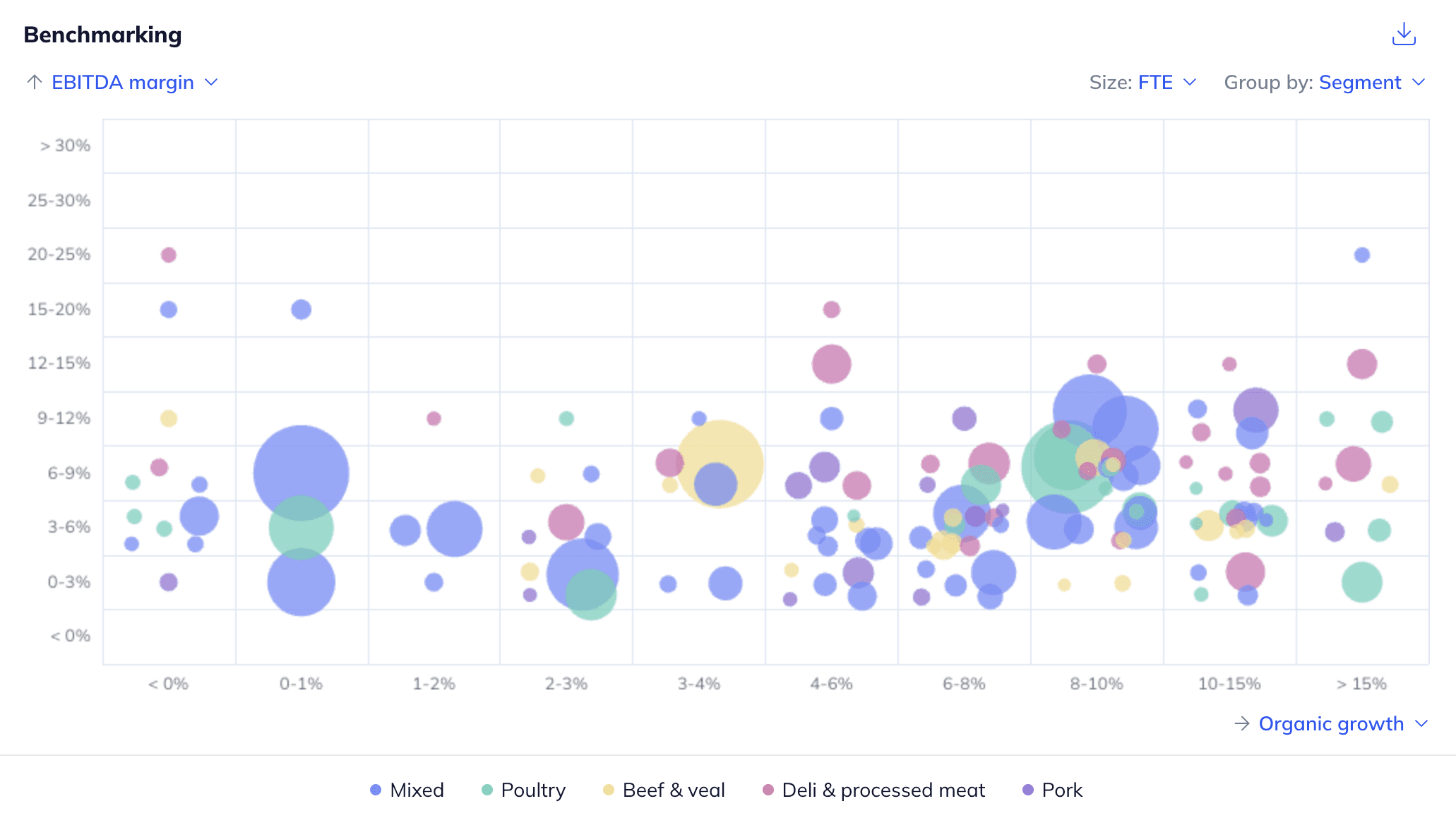

Europe

Companies

200

Table of contents

Statista (August 2024) estimated the European fresh and processed meat market at ~€350bn in 2023 and forecasted it to grow to ~€465bn by 2029 (+5% CAGR)

Meat consumption in Europe amounted to ~53kg per capita in 2024 and was estimated to decline to ~52kg per capita by 2033, registering -0.3% CAGR over the period (OECD, March 2025)

Growing global population and disposable income, particularly in Asia and Africa, paired with intensifying urbanisation and fast-food development in emerging economies will fuel demand for meat imports from Europe (European Commission, January 2025; OECD-FAO, July 2023)

Growing religious diversity and consumers favouring leaner and less resource-intensive poultry meat will continue to provide growth opportunities for European poultry meat producers (The Poultry Site, November 2024)

Development related to improved animal genetics, farm management and better feed formulations allow players to increase breeding rates and animal slaughter weight (OECD-FAO, July 2024; OECD-FAO, June 2021)

Declining red meat consumption in Europe amid growing popularity of vegetarian, vegan and other alternative diets. To illustrate, ~51% of meat consumers have reduced their meat intake in 2023, particularly in Germany, France and Italy (GFI Europe, November 2023; European Commission, January 2025; proveg international, February 2024)

Geopolitical tensions related to armed conflicts (e.g. Russian invasion of Ukraine) and potential tariffs, as well as animal disease outbreaks negatively affect meat production, internal EU demand and exports (FeedNavigator, March 2025; IICA, February 2023; European Commission, January 2025)

EU regulations on sustainable farming threaten the profitability through incremental investments and compliance costs. This is combined with disruptions of farming cycles, water supplies and yield crops caused by global warming (European Commission, January 2025; FAIRR, May 2022; Le Monde, October 2024)

With the full report, you’ll gain access to:

Detailed assessments of the market outlook

Insights from c-suite industry executives

A clear overview of all active investors in the industry

An in-depth look into 200 private companies, incl. financials, ownership details and more.

A view on all 338 deals in the industry

ESG assessments with highlighted ESG outperformers