Industry research

Scope

US

Companies

123

Table of contents

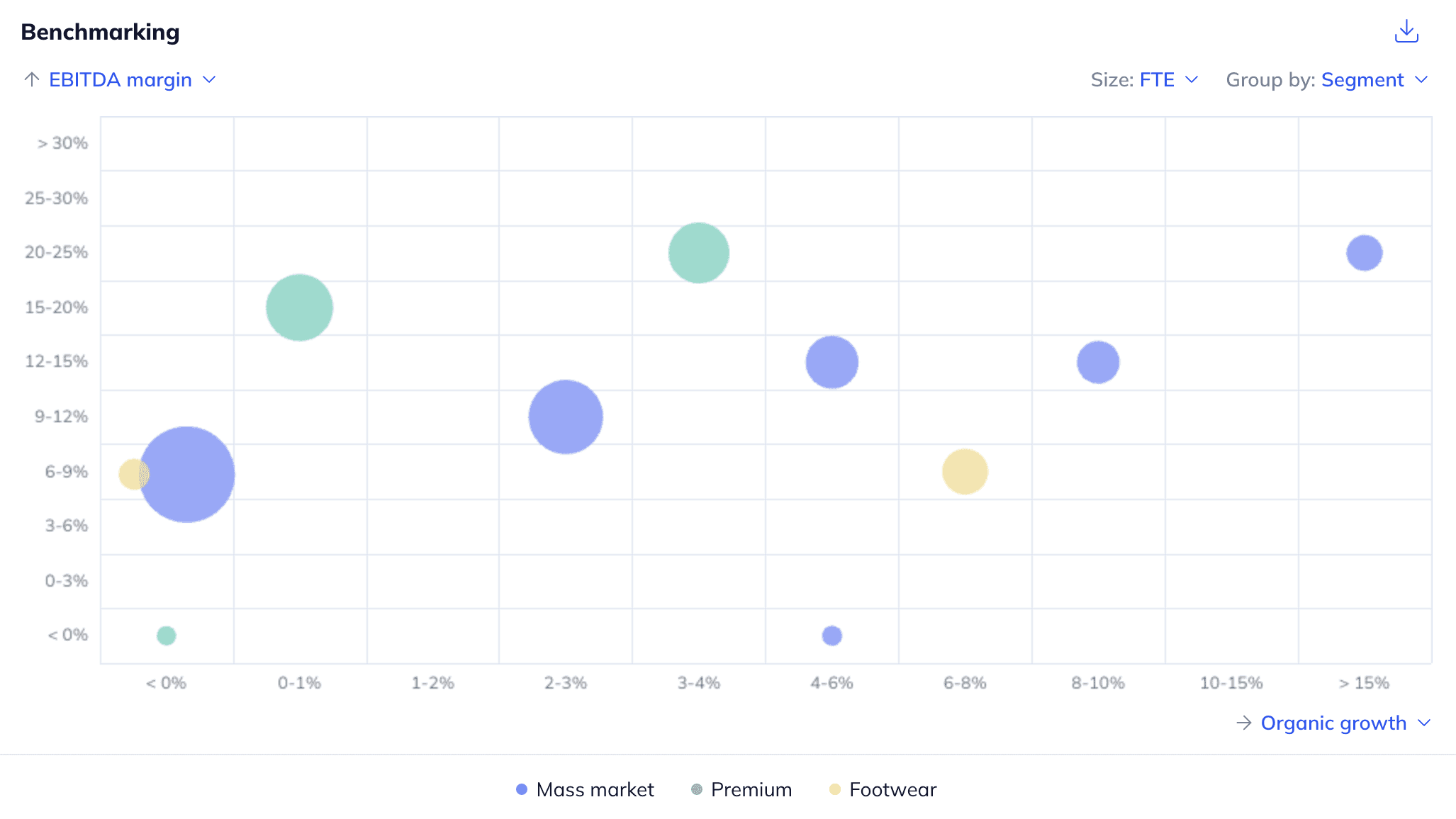

What does the Fashion Brands market landscape look like in the US?

The US fashion brands market exhibits varying levels of fragmentation. While the premium segment is top-heavy, led by a handful of global conglomerates, the mass market segment is more fragmented and the footwear segment is moderately consolidated. Herein, brands deploy various strategies to differentiate themselves and remain competitive. Larger brands rely on M&A to scale and expand capabilities, while smaller brands rely on specializing in niches to compete. Marketing is crucial in this industry, with brands leveraging social media and influencer marketing to capture customer attention. Additionally, distribution strategies dictate margins with players moving towards a higher D2C mix to improve control and boost margins.

What is the level of investor activity in the US Fashion Brands industry?

Sponsor-led interest has been moderate, with ~30% of identified assets being backed by financial sponsors (as of April 2025). Herein, the footwear segment stands out with sponsor interest at ~50% (as of April 2025). In general, investors are primarily drawn to (i) the increasing share of D2C sales, resulting in higher margins, as well as (ii) technological advancement to improve efficiency and personalization trends allowing for premiumization opportunities. On the other hand, (i) the proliferation of counterfeit products, (ii) dynamic consumer preferences leading to excess inventory and potential brand obsoletion, (iii) trade wars and tariffs leading to supply chain disruption and (iv) increased use of resale and rental apparel cannibalizing new product sales act as detractors of investment.

What are the key ESG considerations in the US Fashion Brands industry?

ESG topics in the US fashion brands industry revolve around environmental and social aspects. Environmental issues include high carbon emissions and waste generation from unsustainable fast fashion trends, excessive plastic-based textile and leather use contributing to microplastic pollution and reliance on non-renewable resources for production. To address these issues, companies introduce recycling initiatives and water conservation measures and phase out hazardous materials. On the social side, labor exploitation, unsafe working conditions and forced labor remain prevalent in global supply chains. Remedies involve establishing robust supplier codes of conduct, ensuring fair wages and enforcing ethical labor practices throughout production networks.

The global apparel market is expected to generate ~$1.8tn in revenue in 2025 and is projected to grow to ~$2.0tn in value by 2028 (+2.8% CAGR 2025-2028). Herein, the US apparel market is anticipated to expand from ~$365.7bn in 2025 to ~$389.3bn over the same period (+2.1% CAGR 2025-2028; UniformMarket, February 2025)

RunRepeat (September 2023) forecasts the US footwear market to grow from ~$88.5bn in 2023 to ~$104.1bn in value by 2028 (+3.3% CAGR 2023-2028)

Increased adoption of omnichannel distribution models will boost efficiency and margin growth for US apparel and accessories producers. Brands increasingly implement BOPIS (buy online, pick up in-store) and real-time inventory management to streamline logistics and enhance consumer convenience (BigCommerce, July 2022)

Advancements in production automation and AI-driven design will continue to shorten production and fulfillment cycles. Brands leveraging AI-powered analytics and rapid production networks can pinpoint emerging trends faster, reduce costs and bring fresh designs to market nearly instantly (Cleverence, March 2025)

Increasing demand for unique, personalized fashion experiences allows for margin expansion. Incumbents increasingly embrace AI and 3D-powered made-to-order (MTO) and made-to-measure (MTM) systems to offer bespoke designs at scale. As technology advances, personalized fashion will become even more accessible, fueling deeper consumer engagement and increased profitability (3DLOOK, August 2024)

Growing consumer expectations related to sustainability and ethical sourcing will increasingly disadvantage brands that fail to meet these expectations. As Gen Z and Millennial shoppers prioritize eco-friendly products and transparent supply chains, companies relying on traditional production and procurement practices risk declining market share. Adapting to these demands will increase complexity and raise costs, pressuring margins (Plastiks, February 2025)

The proliferation of highly realistic counterfeit products threatens a decline in brand prestige and customer confidence. As AI-driven technologies enable the creation of indistinguishable knockoffs and unauthorized sellers flood digital marketplaces, consumers will increasingly question product authenticity, affecting pricing power and exclusivity (Potter Clarkson, March 2024)

The accelerating shift toward rental, subscription and resale fashion models poses a growing threat to revenue growth. Herein, Rent the Runway (US) and Nuuly (US) enable consumers to easily access premium fashion without paying full prices, while platforms such as ThredUp (US) and The RealReal (US) further divert spending toward convenient secondhand alternatives. As more brands launch their own resale initiatives, they risk permanently cannibalizing demand for new products while increasing logistical complexities (Business Wire, March 2025; Vogue, November 2024; Trove, November 2024; PYMNTS, April 2024)

With the full report, you’ll gain access to:

Detailed assessments of the market outlook

Insights from c-suite industry executives

A clear overview of all active investors in the industry

An in-depth look into 123 private companies, incl. financials, ownership details and more.

A view on all 212 deals in the industry

ESG assessments with highlighted ESG outperformers