Industry research

Scope

US

Companies

58

Table of contents

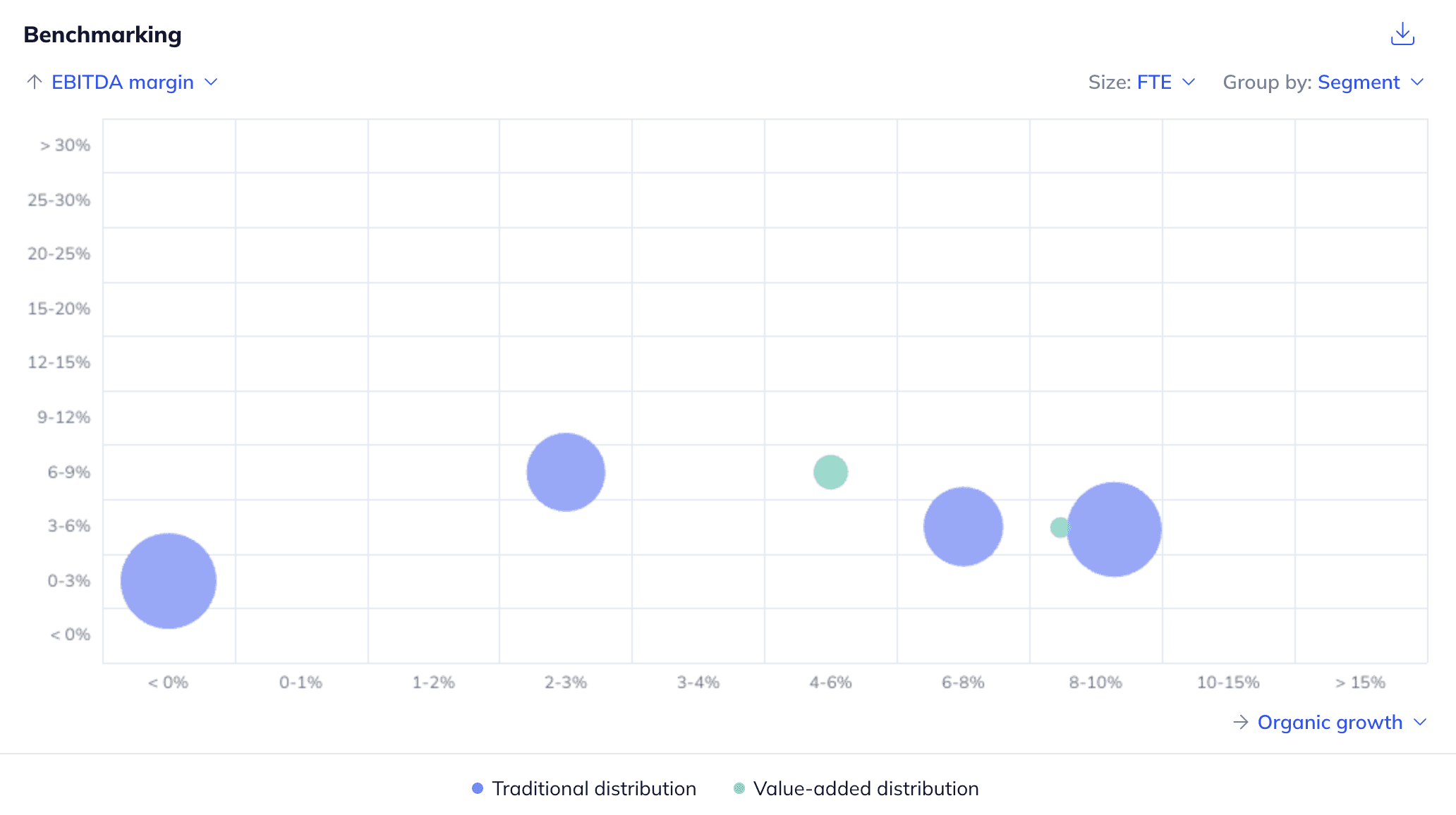

What does the IT Distribution market landscape look like in the US?

The US IT distribution market has few large incumbents who demonstrate strong international footprints, while smaller players have a local focus with niche technology offerings. Established players tend to position themselves as generalists, having an extensive product offering from multiple OEMs to provide customers with a broad range of options. Contrarily, smaller regional players typically focus on a portfolio of products from one or two vendor partners. Barriers to entry are relatively low, primarily due to non-exclusive distribution rights, which are also generally short-term in nature. Incumbents seek to entrench their market positions through preferred vendor statuses and engineering certifications for implementation and strong relationships with leading hardware manufacturers and software developers. Given the rise in complexity related to digital transformation, identified players can capitalize on additional growth avenues by expanding into value-added services (i.e. implementation and maintenance).

What is the level of investor activity in the US IT Distribution industry?

Investor-led interest has been low, with ~16% of identified US assets being backed by financial sponsors (March 2025). Herein, investor interest is fueled by the rising demand for IT equipment on the back of the ongoing digitalization and advancements in AI computing requirements, as well as shorter product lifecycles. Investor activity in the circular IT distribution segment is primarily driven by increasing awareness of environmental sustainability, as well as by aligning with IT hardware OEMs’ circularity targets. The main detractors relate to intense competition, ongoing trade tensions and traditionally meager EBITDA margins.

What are the key ESG considerations in the US IT Distribution industry?

ESG topics relate to environmental, social and governance aspects. Herein, environmental topics include carbon emissions, resource utilization, packaging and electronic waste management. Industry initiatives focus on mitigating environmental impact through responsible end-of-life IT equipment management, recycling and refurbishment programs. Social issues primarily revolve around ethical sourcing and working conditions throughout the supply chain. To mitigate these risks, incumbents operate facilities that are third-party certified for health and safety. Governance issues relate to data security breaches. Identified players ensure safe data handling and wiping compliance through data sanitization, resetting devices and physical destruction procedures.

The US computing market is expected to generate ~$38.9bn in revenue in 2025 and is forecasted to reach ~$40.5bn in revenue in 2029 (Statista, June 2024)

Global IT spendings are expected to rise from ~$5.1tn in 2024 to ~$5.6tn in 2025, demonstrating ~9.8% YoY growth (Gartner, January 2025)

Rising IT spending focused on automation, AI, IoT, security software and digital transformation is poised to drive the demand for IT hardware and software products (Businesswire, May 2024). As businesses struggle with complex integrations, it enables distributors to expand into specialized hardware products (e.g. low-power microcontrollers for IoT devices, AI GPUs for advanced workloads) along with value-added services to bridge the gap (ECS, March 2025)

Lagging digitalization of SMEs results in opportunities for value-added distributors to play a key role in helping SMEs adopt new technologies, aiding growth and digital transformation. To illustrate, ~67% of SMEs struggle to remain competitive, highlighting the need for digital transformation to boost productivity, attract talent and improve efficiency (World Economic Forum, July 2023)

IT OEMs increasingly design products for easier repair and recycling while prioritizing material recovery at end-of-life. This shift leads to increased opportunities for circular IT players by enabling easier refurbishment, remanufacturing and component reuse (Redington, January 2025; Bain & Company, September 2022)

IT manufacturers increasingly leverage e-commerce platforms and demand-creation initiatives to bypass traditional distribution channels, with some OEMs nearly doubling their direct sales share and achieving significant revenue growth, thereby diminishing the role of traditional distributors (McKinsey & Company, October 2023; Digital Commerce 360, November 2023)

Ongoing trade tensions and the unpredictable implementation of new tariffs have led to increased costs for electronic products. Retailers have warned that these additional expenses may be passed on to consumers, potentially dampening demand for IT products and affecting the sales volumes managed by distributors (Wall Street Journal, March 2025)

Rising cybersecurity threats require IT distributors to invest in security measures to prevent data breaches. Breaches from mishandled end-of-life electronic equipment exacerbate challenges for incumbents to maintain chain of custody controls for audit and tracking details to comply with data sanitization laws (World Economic Forum, February 2025; Apto Solutions, December 2023; Insurance Journal, September 2023)

With the full report, you’ll gain access to:

Detailed assessments of the market outlook

Insights from c-suite industry executives

A clear overview of all active investors in the industry

An in-depth look into 58 private companies, incl. financials, ownership details and more.

A view on all 113 deals in the industry

ESG assessments with highlighted ESG outperformers