Industry research

Scope

US

Companies

200

Table of contents

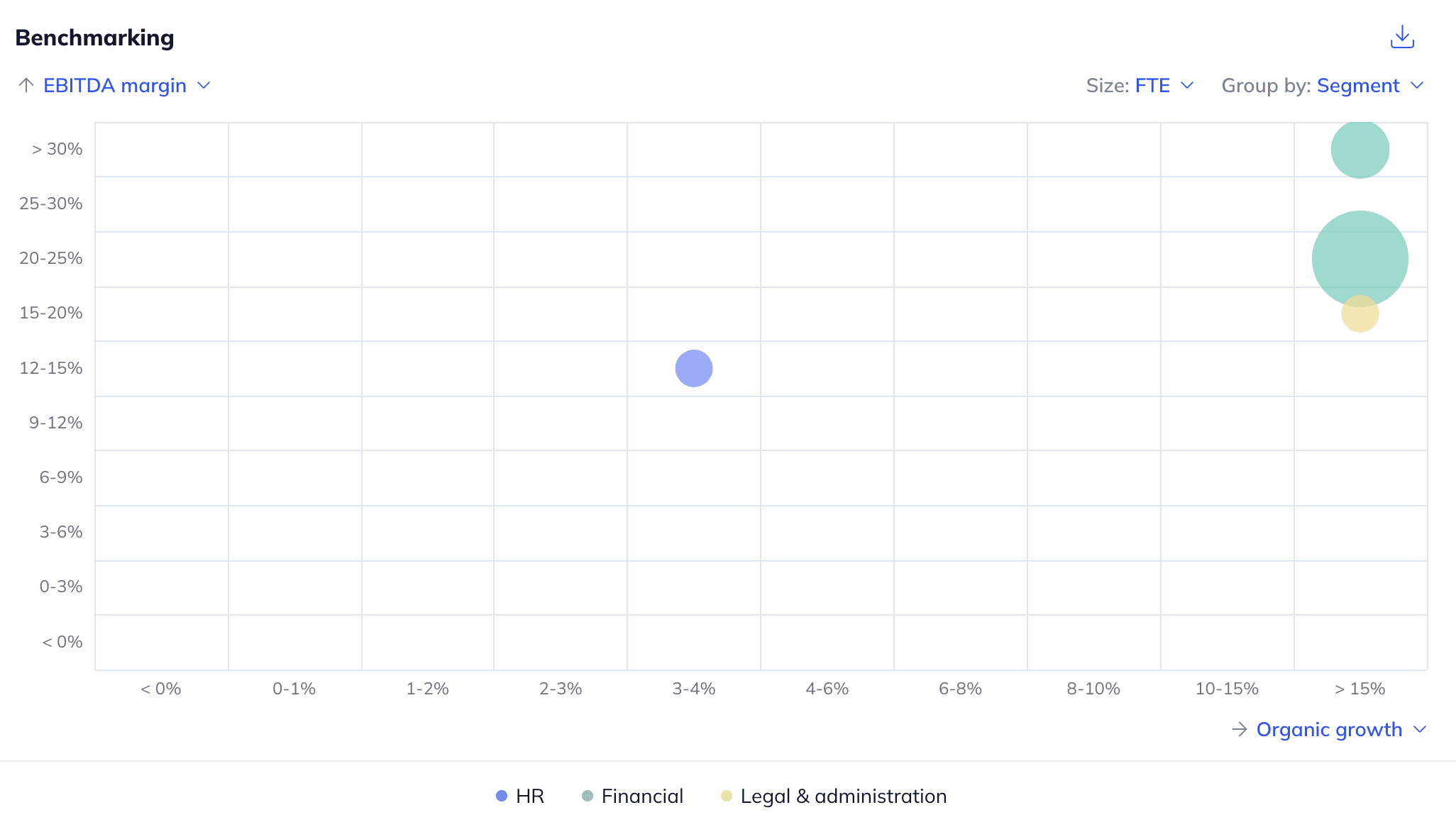

What does the Healthcare BPO market landscape look like in the US?

Consolidation in the US healthcare BPO market varies per segment. Herein, the US healthcare staffing market is relatively more consolidated, with Aya Healthcare, AMN Healthcare and Medical Solutions, forming the top 3 and together holding a ~28% market share in 2022. On the other hand, the financial, legal & administration and marketing segments are significantly more fragmented and face competition from diversified healthcare providers (i.e. hospitals, pharmaceutical distributors) such as McKesson Corporation (US) and HCA Healthcare (US). They also compete with healthcare IT firms such as Veradigm (US), IQVIA (US) and Oracle (Cerner; US) and diversified professional services firms, including Accenture (IE), Genpact (US) and Cognizant (US). Large incumbents continue to innovate through investments in technology (e.g. AI) and expand their presence through M&A. To compete with the large players, smaller incumbents focus on specific geographical regions and specialize in particular niches. For example, Keplr Vision offers non-clinical administrative support services to optometry practices, while AMEA Healthcare provides healthcare staffing services primarily in Ohio.

What is the level of investor activity in the US Healthcare BPO industry?

Investor-led interest has been moderate, with ~39% of identified assets being backed by financial sponsors (as of March 2025). Deterring factors for investors include (i) complex and constantly evolving healthcare regulations at local, state and federal levels, (ii) anticipated Medicaid cuts reducing demand for BPO services and (iii) the growing shortage of skilled healthcare BPO workers. On the flip side, potential sponsor interest stems from (i) the growth in outsourcing of non-essential tasks, enabling physicians to focus on patient care and reduce operational costs, (ii) the emergence and adoption of AI, machine learning and data analytics, which enable healthcare BPOs to navigate reimbursement processes and reduce errors and inefficiencies and (iii) the aging US population and rising chronic conditions, which boost healthcare demand and subsequently for BPO services.

What are the key ESG considerations in the US Healthcare BPO industry?

ESG topics in the US healthcare BPO market primarily revolve around social and governance positive aspects and challenges. Social aspects primarily relate to the impact on patient well-being. Herein, healthcare BPOs improve patient engagement by allowing medical professionals to focus more on patient care, with services such as medical transcriptions ensuring accurate documentation and better communication. At the same time, substandard management or lack of oversight can lead to privacy violations, delayed treatments and compromised patient trust. Other social challenges include work-life balance (e.g. long and irregular hours) and limited career growth opportunities for employees. Herein, incumbents aim to address these issues by providing comprehensive training programs to upskill employees and offering flexible remote work options to maintain work-life balance. Governance issues primarily relate to data protection of highly sensitive patient information, as failure to do so can lead to customer churn, legal disputes and costly litigation. To address this, incumbents incorporate practices such as HIPPA-compliant offerings, data encryption protocols, controlled access, regular audits and employee training to mitigate security risks.

Statista (April 2024) forecasts the US BPO market to reach ~$152.8bn in size in 2025 and projects it to grow to ~$178.7bn by 2029 (+4.0% CAGR 2025-2029)

The US healthcare spending (e.g. hospital care, physician services and healthcare-related IT services) is expected to grow by ~5.6% YoY until 2032, while Medicare spending is projected to increase by ~7.4% YoY until 2032 (AMN Healthcare, February 2025)

The ongoing US healthcare worker shortage drives the need for more efficient administrative healthcare processes and reduced operational costs. To illustrate, Mercer projects a shortage of ~100k healthcare workers in the US by 2028. Herein, outsourcing non-essential tasks such as staffing, marketing and claim processing, can streamline workflows, reduce administrative burdens and allow physicians to focus on patient care (Mercer, August 2024; HelpSquad, April 2024; BCG, January 2024)

The emergence and adoption of AI, machine learning and data analytics helps healthcare BPOs streamline reimbursement processes and reduce errors and inefficiencies. To illustrate, a survey by MIT found that ~80% of medical institutions believe AI boosts their bottom-line, while ~81% say it enhances competitiveness (Commerce Healthcare, January 2025; Avendus, December 2024; Unity Communications, November 2024; MIT News, June 2024)

The aging US population and increased demand from individuals with chronic conditions (e.g. cancer) indirectly expands the demand for BPO services to handle administrative overload while ensuring compliance with stringent regulations (e.g. HIPAA). For example, the 85+ age group in the US is projected to more than double, from ~6.7m in 2020 to ~14.4m by 2040 (interview by Gain.pro, Credence Global Solutions, September 2024; Trualta, June 2023)

The constantly evolving healthcare regulations at local, state and federal levels create uncertainty and increase operational costs for healthcare BPO companies. These regulations also restrict access to consumer information, limit re-targeting, ban physical referrals and impose budget constraints, complicating operations for healthcare BPO providers (interview by Gain.pro; Avendus, December 2024; Social Climb, January 2024; TimesPro, June 2023)

Medicaid beneficiaries are expected to decline in 2025 due to eligibility redetermination, while the Trump administration's planned ~$800bn Medicaid budget cut could leave ~20m people without coverage. This may reduce demand for Medicaid-related BPO services and prompt cost-cutting measures and renegotiated BPO contracts by healthcare organizations (interview by Gain.pro; Medicare Rights, February 2025; The Guardian, February 2025)

The growing shortage of skilled healthcare BPO workers in the US hampers the industry's ability to meet demand, driving up costs and limiting capacity. Herein, the integration of advanced data analytics and technology in healthcare BPO could require specialized skills, potentially increasing staffing costs as companies seek to attract and retain skilled professionals (Unity Communications, November 2024; ScaleHub, March 2022)

With the full report, you’ll gain access to:

Detailed assessments of the market outlook

Insights from c-suite industry executives

A clear overview of all active investors in the industry

An in-depth look into 200 private companies, incl. financials, ownership details and more.

A view on all 427 deals in the industry

ESG assessments with highlighted ESG outperformers